The Process Involved When You Decide to Purchase Reverse Mortgage

Wiki Article

Discover the Conveniences of Investing In a Reverse Home Mortgage Today

A reverse mortgage presents a viable solution, permitting people aged 62 and older to transform their home equity right into money, hence alleviating financial burdens without requiring monthly settlements. Recognizing the subtleties and ramifications of this option is essential, as it might dramatically influence future monetary stability.What Is a Reverse Home Mortgage?

A reverse home loan is a financial item developed to aid house owners aged 62 and older use their home equity without having to market their building. This distinct lending allows qualified house owners to transform a part of their home equity right into cash money, which can be made use of for different purposes, consisting of covering living expenditures, health care prices, or home adjustments.Unlike typical home loans, where month-to-month repayments are made to the lending institution, reverse home loans call for no monthly payment. Rather, the funding is settled when the property owner markets the home, leaves, or dies. The quantity owed normally includes the preliminary loan quantity, accrued rate of interest, and any charges. Notably, homeowners keep title to their residential or commercial property throughout the financing period and are in charge of real estate tax, insurance coverage, and maintenance.

There are numerous kinds of reverse home mortgages, consisting of Home Equity Conversion Home Mortgages (HECM), which are government guaranteed. Qualification is based upon the house owner's age, home equity, and creditworthiness. This financial tool provides a practical choice for elders looking for monetary versatility while staying in their homes, making it an increasingly popular choice amongst senior citizens.

Financial Freedom in Retired Life

Accomplishing financial independence in retirement is an objective for several senior citizens, and reverse home loans can play a critical duty in this quest. This monetary instrument allows property owners aged 62 and older to transform a section of their home equity right into cash money, supplying a consistent earnings stream without the obligation of month-to-month home mortgage repayments.For retirees, preserving financial freedom usually copyrights on having access to enough resources to cover unexpected prices and daily expenditures. A reverse home loan can aid link the gap in between fixed earnings resources, such as Social Safety and pensions, and increasing living expenditures, including medical care and real estate tax. By using the equity in their homes, seniors can improve their capital, permitting them to live more conveniently and with higher security.

Moreover, reverse mortgages can empower senior citizens to make options that straighten with their way of living goals, such as funding traveling, taking part in hobbies, or sustaining family members - purchase reverse mortgage. With cautious planning and factor to consider, a reverse mortgage can act as a beneficial tool, making it possible for retirees to accomplish their wanted quality of life while maintaining their freedom and self-respect throughout their retirement years

Accessing Home Equity

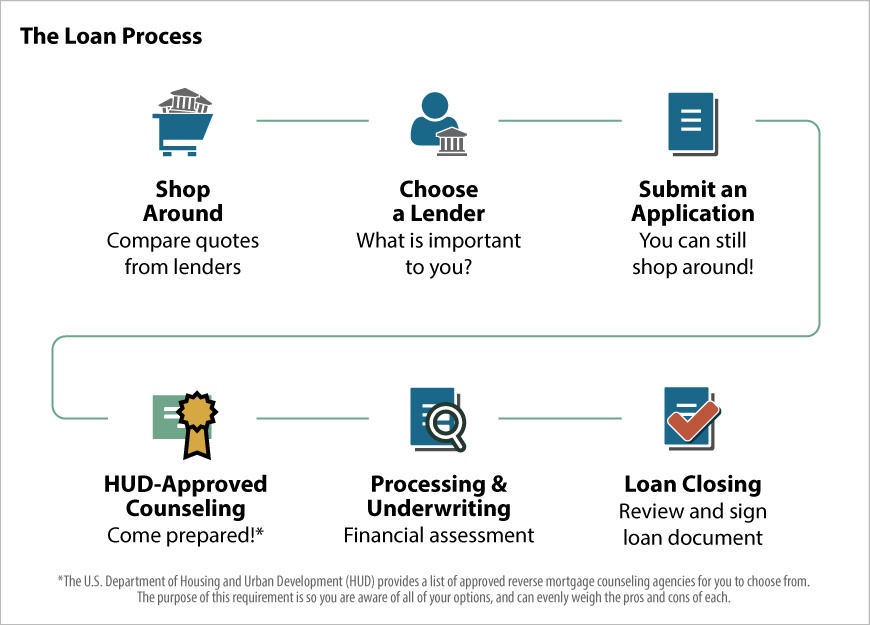

Homeowners aged 62 and older have a special possibility to access a significant part of their home equity with reverse home loans, boosting their monetary adaptability in retirement. This financial product permits qualified elders to transform a section of their home equity right into cash, offering funds that can be used for different functions, such as healthcare expenses, home alterations, or daily living expenses.The procedure of getting a reverse mortgage commonly includes a straightforward application and approval method. As soon as safeguarded, home owners can receive their equity in numerous types, consisting of a round figure, regular monthly settlements, or a credit line. This flexibility allows retired people to tailor their financing according to their details demands and conditions.

Notably, reverse home loans are non-recourse financings, suggesting that debtors will never owe greater than the worth of their home at the time of settlement, even if the loan balance goes beyond that worth. This attribute uses tranquility of mind, making certain that retired life cost savings are protected. Accessing home equity via a reverse home mortgage can serve as a vital monetary strategy, making it possible for older adults to delight in a more comfortable and secure retirement while leveraging the wide range tied up in their homes.

Getting Rid Of Monthly Home Loan Payments

One of one of the most significant benefits of a reverse home mortgage is the elimination of regular monthly home mortgage payments, supplying homeowners with instant financial relief. This helpful hints attribute is particularly valuable for retirees or those on a set revenue, as it reduces the worry of monthly monetary obligations. By converting home equity right into accessible funds, property owners can reroute their sources towards essential living expenditures, healthcare, or personal undertakings without the tension of maintaining regular home loan settlements.Unlike conventional home loans, where month-to-month payments add to the principal balance, reverse home loans operate a various concept. House owners retain ownership of their residential property while gathering interest on the car loan amount, which is only repaid when they sell the home, leave, or die. This one-of-a-kind setup enables individuals to remain in their homes longer, boosting economic stability throughout retired life.

Additionally, the absence of month-to-month home mortgage settlements can substantially enhance money flow, making it possible for property owners to handle their spending plans better. This financial adaptability encourages them to make far better way of living options, purchase chances, or simply enjoy an extra comfortable retired life without the continuous issue try this web-site of mortgage payment obligations (purchase reverse mortgage). Thus, the removal of monthly settlements sticks out as a fundamental advantage of reverse mortgages

Enhancing Top Quality of Life

A significant advantage of reverse home loans is their ability to dramatically enhance the lifestyle for retired people and older homeowners. By converting home equity right into easily accessible cash, these monetary products provide a crucial source for taking care of everyday expenditures, clinical expenses, and unanticipated prices. This financial versatility enables seniors to maintain their wanted standard of living without the concern of month-to-month home loan payments.In addition, reverse home loans can empower house owners to go after individual rate of interests and leisure activities that might have been previously unaffordable. Whether it's taking a trip, taking courses, or involving in social tasks, the supplemental revenue can foster an extra meeting retired life experience.

In addition, reverse home mortgages can be critical in addressing healthcare demands. Several retired people deal with increasing medical expenses, and having extra funds can facilitate prompt treatments, medications, or even home modifications to accommodate movement difficulties.

Conclusion

Unlike traditional home loans, where monthly settlements are made to the loan provider, reverse home mortgages call for no monthly settlement.There are numerous kinds of reverse mortgages, consisting of Home Equity Conversion Mortgages (HECM), which are federally insured. Accessing home equity with a reverse home mortgage can offer as an essential monetary strategy, allowing older adults to appreciate a much more safe and secure and comfortable retired life while leveraging the riches connected up in their homes.

One of the most significant benefits of a reverse home loan is the elimination of additional reading regular monthly home loan repayments, offering homeowners with prompt financial relief.Unlike typical home loans, where monthly settlements add to the principal equilibrium, reverse home mortgages operate on a different principle.

Report this wiki page